Dispersion or variation is very useful in the application of advanced statistical techniques like correlation, regression analysis of time series, tests of significance etc. Also useful in determining the effective production control techniques.

Tuesday, 6 December 2016

B1 Statistics 16 Measures of variation or Dispersion

Need for Dispersion: -

Though the averages serve the purpose of describing the characteristics of the distribution, they cannot give a comprehensive idea and as such conceal many important facts about the distribution. One of the important aspects concealed by measures of central tendency is regarding the variability in the values. It fails to explain the extent of deviation from the average value in the given distribution. In the absence of such information. The averages among the different distributions cannot be meaningfully compared.

Then the need of measures of central tendency or other measures like dispersion and skewness are devised.

Measures of dispersion explain the degree of variation in the individual items from the central value, the skewness measures the degree of symmetry of asymmetry of the distribution.

The need for the measurement of dispersion when the averages are same but the variations in the individual items are different.

Thursday, 1 December 2016

A3 15 DISSOLUTION OF FIRM

SECTION 39 TO 55 of the partnership Act, 1932 contains the provisions of dissolution

A3 Ascertaining the amount due to the retiring / deceased partner

The total amount payable comprises the following:

1. Capital Account Balance

2.Interest on Capital and salary, if any upto the date of retirement/death

3.Share of accumulated profits/losses.

4.Share of Profit/loss on revaluation

5.Share of Good will

6.Share of profit/loss for the current period, i.e from the date of last preparation of final accounts to the date of retirement/death.

1. Capital Account Balance

2.Interest on Capital and salary, if any upto the date of retirement/death

3.Share of accumulated profits/losses.

4.Share of Profit/loss on revaluation

5.Share of Good will

6.Share of profit/loss for the current period, i.e from the date of last preparation of final accounts to the date of retirement/death.

A3 Fixed and current Capital method

Capital acct as well as current accounts of the partners are maintained to show the amount of the capital contributed by the partners. Current acct show other items like drawings interest on capital etc

A3 Floating capital method

Capital acct is kept for each partner and the capital will be fluctuating from one period to another.

Monday, 13 June 2016

Friday, 10 June 2016

C3 Purchasing procedure

Purchasing procedure

1. Receiving the indents or purchase requisition

2. Ascertainment of possible sources of supply and selection of a particular supplier.

3. Placing purchase order on supplier

4. Follow-up of Purchase order

5. Receiving and inspection of materials

6. Verification and passing of supplier s invoice for payments

1. Receiving the indents or purchase requisition

2. Ascertainment of possible sources of supply and selection of a particular supplier.

3. Placing purchase order on supplier

4. Follow-up of Purchase order

5. Receiving and inspection of materials

6. Verification and passing of supplier s invoice for payments

C3 FUNCTIONS OF PURCHASE DEPARTMENT

FUNCTIONS OF PURCHASE DEPARTMENT

Routine Functions

1. collection and registrations of purchase requisitions or indents from the stores department and for special and urgent materials from production and consuming department

2. Ascertainment of the possible sources of supply of required materials

3. selection of right suppliers

4. placing the purchase order

5. Follow-up of the purchase order to avoid any delay in delivery

6. obtaining goods received note and inspection note to ensure that quantity and quality of materials received are according to PO

7. Returning materials which are not according to specifications or securing adjustments with the supplier on claims for discrepancies

8. Verifying the invoice with regard to quality, price and other relevant particulars and pass it for payment and sending the invoice to the accounts section.

Some other functions are

1.To collect maintain proper records and documents like catalogues, price lists,, trade magazines and journals to assist in locating the best market.

2. To develop and maintain good supplier relations

3. to serve as an information centre on materials

4. to develop standard forms and document used in purchasing process.

5.TO prepare purchase budget

Routine Functions

1. collection and registrations of purchase requisitions or indents from the stores department and for special and urgent materials from production and consuming department

2. Ascertainment of the possible sources of supply of required materials

3. selection of right suppliers

4. placing the purchase order

5. Follow-up of the purchase order to avoid any delay in delivery

6. obtaining goods received note and inspection note to ensure that quantity and quality of materials received are according to PO

7. Returning materials which are not according to specifications or securing adjustments with the supplier on claims for discrepancies

8. Verifying the invoice with regard to quality, price and other relevant particulars and pass it for payment and sending the invoice to the accounts section.

Some other functions are

1.To collect maintain proper records and documents like catalogues, price lists,, trade magazines and journals to assist in locating the best market.

2. To develop and maintain good supplier relations

3. to serve as an information centre on materials

4. to develop standard forms and document used in purchasing process.

5.TO prepare purchase budget

C3 IMPORTANT ASPECTS OF MATERIAL COST CONTROL

IMPORTANT ASPECTS OF MATERIAL COST CONTROL

1. Purchasing of materials should be made by proper authority

2. Receiving and Inspection, recording and proper storage of material must be ensured.

3. Storing and

4. Production

5. issues should be based on authorised requisitions in writing from the needy departments

6.Adequate storage facilities must be made available

1. Purchasing of materials should be made by proper authority

2. Receiving and Inspection, recording and proper storage of material must be ensured.

3. Storing and

4. Production

5. issues should be based on authorised requisitions in writing from the needy departments

6.Adequate storage facilities must be made available

C3 OBJECTIVES OF MATERIAL CONTROL

OBJECTIVES OF MATERIAL CONTROL

1. Ensure availability of material.

2. Preserving the material by eliminating wastages

3. Adopting a system of perpetual inventory and timely reporting to management accurate information

4. Avoid over stock

5. Ensure right quality at right price

6. Keep the lowest carrying cost as far as possible.

7. Minimum cost of storage

1. Ensure availability of material.

2. Preserving the material by eliminating wastages

3. Adopting a system of perpetual inventory and timely reporting to management accurate information

4. Avoid over stock

5. Ensure right quality at right price

6. Keep the lowest carrying cost as far as possible.

7. Minimum cost of storage

C3 ELEMENTS OF COST

ELEMENTS OF COST

Two Types: Direct costs and indirect costs

Direct Material

raw materials,Semi-finished materials or components which become part ad parcel of the product are known as direct material.

E.g clay in bricks

wood in furniture

leather in shoe

cotton in yarn etc.

However if a material forms part of the product but is of a negligible value, it may be treated as indirect material.

E.g yarn used in making shoes

nails used in furniture making etc.

Direct Labour

labour which can be conveniently identified with and directly charged to a particular product, job, service etc. it is all labour which is expended in converting raw materials into finished products.

E.g

wages paid to labour engaged in the actual production or carrying out an operation or process or a contract.

also called direct wages, productive labour, operating labour, prime cost labour etc.

Direct Expenses

All expenses other than direct material and direct labour which can be conveniently identified with or directly chargeable to a product, job, process or service are called direct expenses. Also called chargeable expenses, prime cost expenses and productive expenses.

E.g

Cost of special patterns, designs, drawings and tools made or purchased for specific product or process, excise duty, royalty, architects feesm and hore charges of special tools and equipment used for a particular product, job or service.

Indirect Material

Material which cannot be traced in and which does not form part of the finished product. it cannot be directly charged to a particular cost centre, product, job, contract process etc.

E.g

consumable stores

lubricants

cotton waste

grease oils

chemicals added in process etc.

Indirect Labour

Cost of labour which cannot be identified with or directly charged to a product, job, process or service etc. and which is general in nature is called indirect labour. it represents cost of labour expended on auxiliary work in connection with the product manufactured. it aids and facilitated production work indirectly.

E.g wages paid to maintenance workers employed in workshops,

mechanics, cleaners, store-keepers, watch and ward and clerical staff etc.

Indirect Expenses

Expenses which cannot be directly charged to production and which are other than indirect and indirect material are called indirect expenses.

E.g

Rent

rates

insurance

taxes

power,lighting

heating, repairs , canteen expenses, hospital and dispensary expenses

office and administrative expenses, etc.

Two Types: Direct costs and indirect costs

Direct Material

raw materials,Semi-finished materials or components which become part ad parcel of the product are known as direct material.

E.g clay in bricks

wood in furniture

leather in shoe

cotton in yarn etc.

However if a material forms part of the product but is of a negligible value, it may be treated as indirect material.

E.g yarn used in making shoes

nails used in furniture making etc.

Direct Labour

labour which can be conveniently identified with and directly charged to a particular product, job, service etc. it is all labour which is expended in converting raw materials into finished products.

E.g

wages paid to labour engaged in the actual production or carrying out an operation or process or a contract.

also called direct wages, productive labour, operating labour, prime cost labour etc.

Direct Expenses

All expenses other than direct material and direct labour which can be conveniently identified with or directly chargeable to a product, job, process or service are called direct expenses. Also called chargeable expenses, prime cost expenses and productive expenses.

E.g

Cost of special patterns, designs, drawings and tools made or purchased for specific product or process, excise duty, royalty, architects feesm and hore charges of special tools and equipment used for a particular product, job or service.

Indirect Material

Material which cannot be traced in and which does not form part of the finished product. it cannot be directly charged to a particular cost centre, product, job, contract process etc.

E.g

consumable stores

lubricants

cotton waste

grease oils

chemicals added in process etc.

Indirect Labour

Cost of labour which cannot be identified with or directly charged to a product, job, process or service etc. and which is general in nature is called indirect labour. it represents cost of labour expended on auxiliary work in connection with the product manufactured. it aids and facilitated production work indirectly.

E.g wages paid to maintenance workers employed in workshops,

mechanics, cleaners, store-keepers, watch and ward and clerical staff etc.

Indirect Expenses

Expenses which cannot be directly charged to production and which are other than indirect and indirect material are called indirect expenses.

E.g

Rent

rates

insurance

taxes

power,lighting

heating, repairs , canteen expenses, hospital and dispensary expenses

office and administrative expenses, etc.

C3 TECHNIQUES OF COSTING

TECHNIQUES OF COSTING:

1.Marginal Costing:

it is a technique of cost accounting, which ascertains the marginal costs of a product or an operation by differentiating between fixed and variable costs. The technique reveals how volume and costs affect the profit

2. Absorption Costing

Under this technique both fixed and variable costs are charged to operations or processes. This is known as total cost technique. This technique is useful for preparing tenders.

3. Standard Costing

This is a technique of costing in which a comparison is made of the actual cost with predetermined (standard )cost and the deviations if any, are corrected. useful for cost control.

4. Budgetary control

technique of controlling costs by preparing budgets, coordinating activities of various departments, pinpointing their responsibilities and continuous comparison of actual performance with the budgeted.

1.Marginal Costing:

it is a technique of cost accounting, which ascertains the marginal costs of a product or an operation by differentiating between fixed and variable costs. The technique reveals how volume and costs affect the profit

2. Absorption Costing

Under this technique both fixed and variable costs are charged to operations or processes. This is known as total cost technique. This technique is useful for preparing tenders.

3. Standard Costing

This is a technique of costing in which a comparison is made of the actual cost with predetermined (standard )cost and the deviations if any, are corrected. useful for cost control.

4. Budgetary control

technique of controlling costs by preparing budgets, coordinating activities of various departments, pinpointing their responsibilities and continuous comparison of actual performance with the budgeted.

C3 Methods of Costing

Unit costing

costing which can be developed in industries having continuous production, the units of which are identical and standardised.

Job Costing

in which each job is taken as cost unit or a cost centre and it is appropriate for jobbing factories, assembling units etc.

Batch Costing

Extension of Job costing. A batch may represent a number of small orders passed through the factory in batch. Each batch is treated as a cost unit and costs are ascertained separately. it is useful for biscuit, cloth industries.

Contract Costing

Costing in which cost of production is ascertained for each contract, and it is applied to contract and erection industries.

Process Costing

Costing in which the product passes through a series of processes till is completed. and cost is ascertained for each process. it is suitable for industries like chemical, coal, soap. leather, timber etc.

Operating Costing

Costing which is used to ascertain the cost of services rendered. it is suitable for hospitals, hotels, transport, power supply industries.

costing which can be developed in industries having continuous production, the units of which are identical and standardised.

Job Costing

in which each job is taken as cost unit or a cost centre and it is appropriate for jobbing factories, assembling units etc.

Batch Costing

Extension of Job costing. A batch may represent a number of small orders passed through the factory in batch. Each batch is treated as a cost unit and costs are ascertained separately. it is useful for biscuit, cloth industries.

Contract Costing

Costing in which cost of production is ascertained for each contract, and it is applied to contract and erection industries.

Process Costing

Costing in which the product passes through a series of processes till is completed. and cost is ascertained for each process. it is suitable for industries like chemical, coal, soap. leather, timber etc.

Operating Costing

Costing which is used to ascertain the cost of services rendered. it is suitable for hospitals, hotels, transport, power supply industries.

C3 Principles of Cost Accounting

1.For each and every item of cost, cause and effect relationship should be established.

2.Should give factual picture of the profitability of a project.

3.past costs should not be recovered from the future costs.

4.Abnormal cost should not be considered in cost accounting which misleads taking decisions

5.to ensure correctness, cost ledgers and cost control account should be prepared under the principles of double entry

2.Should give factual picture of the profitability of a project.

3.past costs should not be recovered from the future costs.

4.Abnormal cost should not be considered in cost accounting which misleads taking decisions

5.to ensure correctness, cost ledgers and cost control account should be prepared under the principles of double entry

C3 Limitations of Cost Accounting

1. No uniformity in costing systems

2. the application of cost accounting involves too many customs and estimates.

3, it is costly and hence not suitable to small concerns.

4. fails in directing the concern how to face the inflationary conditions in future.

2. the application of cost accounting involves too many customs and estimates.

3, it is costly and hence not suitable to small concerns.

4. fails in directing the concern how to face the inflationary conditions in future.

C3 ADVANTAGES OF COST ACCOUNTING

1. Identifies the profitable and unprofitable activities of a concern

2. provides reliable data r information for managerial decision making

3.it measures organisation efficiency and suggests the measures for improvement

4.helps in preparing renders or quotations

5.ensures future production planning

6.discloses the sources of losses and wastages

7. distinguishes efficient and inefficient workers and encourages efficiency

8.discloses sources of losses and wastages

9. discloses the liquidity and profitability position of the concern

10. helps the government in policy formulation and tax imposition.

2. provides reliable data r information for managerial decision making

3.it measures organisation efficiency and suggests the measures for improvement

4.helps in preparing renders or quotations

5.ensures future production planning

6.discloses the sources of losses and wastages

7. distinguishes efficient and inefficient workers and encourages efficiency

8.discloses sources of losses and wastages

9. discloses the liquidity and profitability position of the concern

10. helps the government in policy formulation and tax imposition.

C3 FINANCIAL ACCOUNTING AND COST ACCOUNTING

S.No

|

Financial Accounting

|

Cost Accounting

|

1

|

Have specific purpose to serve and

kept in manner to present correct

figures to tax authorities. Classification and recording of transactions

directed towards the preparation of final accounts.

|

With collection, classification, analysis and presentation of

costs for the guidance of management for proper planning, organization,

decision making, cost control and policy formulation and for efficient

successful management

|

2.

|

Accounting treat costs in very

broadly

|

Accounting treat costs in greater detail

|

Eg transaction of

material purchased

|

Necessity of material

|

|

3

|

Cannot give reliable and accurate answers needed by

management

|

Indicates the reliable answers for the

queries

|

4

|

Cost of manufacture of products

information will only be totals and too the end of accounting

|

Cost of manufacturing of products may be analyzed in

terms of expenditure, departments or functions

|

5

|

Cannot reveal inefficiencies in material handling

|

reveal inefficiencies in material handling

|

6.

|

Cannot have proper control over

materials and stores, labour

and overheads

|

have proper control over materials and stores, labour

and overheads

|

7.

|

Do not provide detailed classification of expenditure and

draw distinction betweens costs as fixed or variable, controllable or

uncontrollable etc

|

Can provide detailed classification of expenditure and

draw distinction betweens costs as fixed or variable, controllable or

uncontrollable etc

|

8.

|

Stock is valued at cost at market price which

ever is lower

|

Stock is valued only at cost

|

C3 OBJECTIVES OF COST ACCOUNTING

OBJECTIVES OF COST ACCOUNTING

1. To ascertain the cost of products or services and to determine the selling price

2. To control costs

3. To provide basis for the management of formulate policies and to carry out its functions efficiently

Formulating policies are:

Determination of break even point( where there will be no profit and no loss)

Introduction of new product or new line of production

whether to shut down plant to operate at loss

replacement of existing machines for automation

whether to make or buy utilisation of idle capacity future expansion and development policies and capital outlays and so on.

4.it assists the management in carrying out it functions of planning budgeting, decision making, organising, controlling pricing and evaluating operative efficiency etc.

5. to ascertain the profitable and unprofitable lines of activities

6.to find the causes that lead to profits/losses

7.to provide basis for the preparation of budgets.

8.to check and control all types of wastages

9.to establish effective control over machines , material and overheads.

10. to help in valuation of inventory, productions

1. To ascertain the cost of products or services and to determine the selling price

2. To control costs

3. To provide basis for the management of formulate policies and to carry out its functions efficiently

Formulating policies are:

Determination of break even point( where there will be no profit and no loss)

Introduction of new product or new line of production

whether to shut down plant to operate at loss

replacement of existing machines for automation

whether to make or buy utilisation of idle capacity future expansion and development policies and capital outlays and so on.

4.it assists the management in carrying out it functions of planning budgeting, decision making, organising, controlling pricing and evaluating operative efficiency etc.

5. to ascertain the profitable and unprofitable lines of activities

6.to find the causes that lead to profits/losses

7.to provide basis for the preparation of budgets.

8.to check and control all types of wastages

9.to establish effective control over machines , material and overheads.

10. to help in valuation of inventory, productions

C3 Principle techniques of Costing

The Principle techniques of Costing are:

1. Marginal Costing

2. Standard Costing

3. Absorption Costing

4.Uniform Costing

5. Budgetary control

1. Marginal Costing

2. Standard Costing

3. Absorption Costing

4.Uniform Costing

5. Budgetary control

C3 PRINCIPLE METHODS OF COSTING

PRINCIPLE METHODS OF COSTING

1.JOB COSTING

Batch costing

Terminal or contract costing

Multiple costing etc.

2.PROCESS COSTING

Operation costing

Single or Output costing

operating costing

1.JOB COSTING

Batch costing

Terminal or contract costing

Multiple costing etc.

2.PROCESS COSTING

Operation costing

Single or Output costing

operating costing

C3 COST ACCOUNTANCY DEFINITIONS

COST

An amount of Expenditure incurred on a given thing

COSTING

Technique and process of ascertaining costs

COST ACCOUNTING

Is a formal mechanism by means of which costs of products or services are ascertained and controlled

COST ACCOUNTANCY

Application of costing and cost accounting principles methods and techniques to the science art and practice of cost control and the ascertainment of profitability.

information derived used for managerial decision making

An amount of Expenditure incurred on a given thing

COSTING

Technique and process of ascertaining costs

COST ACCOUNTING

Is a formal mechanism by means of which costs of products or services are ascertained and controlled

COST ACCOUNTANCY

Application of costing and cost accounting principles methods and techniques to the science art and practice of cost control and the ascertainment of profitability.

information derived used for managerial decision making

Thursday, 9 June 2016

C3 Marginal costing cost accounting

Marginal cost is the change in the total cost when the quantity produced is incremented by one. That is, it is the cost of producing one more unit of a good. For example, let us suppose:

Variable cost per unit = Rs 25

Fixed cost = Rs 1,00,000

Cost of 10,000 units = 25 × 10,000 = Rs 2,50,000

Total Cost of 10,000 units = Fixed Cost + Variable Cost

= 1,00,000 + 2,50,000

= Rs 3,50,000

Total cost of 10,001 units = 1,00,000 + 2,50,025

= Rs 3,50,025

Marginal Cost = 3,50,025 – 3,50,000

= Rs 25

Need for Marginal Costing

Let us see why marginal costing is required:

Fixed cost = Rs 1,00,000

Cost of 10,000 units = 25 × 10,000 = Rs 2,50,000

Total Cost of 10,000 units = Fixed Cost + Variable Cost

= 1,00,000 + 2,50,000

= Rs 3,50,000

Total cost of 10,001 units = 1,00,000 + 2,50,025

= Rs 3,50,025

Marginal Cost = 3,50,025 – 3,50,000

= Rs 25

Need for Marginal Costing

Let us see why marginal costing is required:

Variable cost per unit remains constant; any increase or decrease in production changes the total cost of output.

Total fixed cost remains unchanged up to a certain level of production and does not vary with increase or decrease in production. It means the fixed cost remains constant in terms of total cost.

Fixed expenses exclude from the total cost in marginal costing technique and provide us the same cost per unit up to a certain level of production.

Features of Marginal Costing

Features of marginal costing are as follows:

Features of marginal costing are as follows:

Marginal costing is used to know the impact of variable cost on the volume of production or output.

Break-even analysis is an integral and important part of marginal costing.

Contribution of each product or department is a foundation to know the profitability of the product or department.

Addition of variable cost and profit to contribution is equal to selling price.

Marginal costing is the base of valuation of stock of finished product and work in progress.

Fixed cost is recovered from contribution and variable cost is charged to production.

Costs are classified on the basis of fixed and variable costs only. Semi-fixed prices are also converted either as fixed cost or as variable cost.

Ascertainment of Profit under Marginal Cost

‘Contribution’ is a fund that is equal to the selling price of a product less marginal cost. Contribution may be described as follows:

‘Contribution’ is a fund that is equal to the selling price of a product less marginal cost. Contribution may be described as follows:

Contribution = Selling Price – Marginal Cost

Contribution = Fixed Expenses + Profit

Contribution – Fixed Expenses = Profit

Income Statement under Marginal Costing

Income Statement

Contribution = Fixed Expenses + Profit

Contribution – Fixed Expenses = Profit

Income Statement under Marginal Costing

Income Statement

For the year ended 31-03-2014

Particulars Amount Total

Sales 25,00,000

Less: Variable Cost:

Cost of goods manufactured 12,00,000

Variable Selling Expenses 3,00,000

Variable Administration Expenses 50,000

15,50,000

Contribution 9,50,000

Less: Fixed Cost:

Fixed Administration Expenses 70,000

Fixed Selling Expenses 1,30,000 2,00,000

7,50,000

Advantages of Marginal Costing

The advantages of marginal costing are as follows:

Sales 25,00,000

Less: Variable Cost:

Cost of goods manufactured 12,00,000

Variable Selling Expenses 3,00,000

Variable Administration Expenses 50,000

15,50,000

Contribution 9,50,000

Less: Fixed Cost:

Fixed Administration Expenses 70,000

Fixed Selling Expenses 1,30,000 2,00,000

7,50,000

Advantages of Marginal Costing

The advantages of marginal costing are as follows:

Easy to operate and simple to understand.

Marginal costing is useful in profit planning; it is helpful to determine profitability at different level of production and sale.

It is useful in decision making about fixation of selling price, export decision and make or buy decision.

Break even analysis and P/V ratio are useful techniques of marginal costing.

Evaluation of different departments is possible through marginal costing.

By avoiding arbitrary allocation of fixed cost, it provides control over variable cost.

Fixed overhead recovery rate is easy.

Under marginal costing, valuation of inventory done at marginal cost. Therefore, it is not possible to carry forward illogical fixed overheads from one accounting period to the next period.

Since fixed cost is not controllable in short period, it helps to concentrate in control over variable cost.

B3 Cash from operations

In Balance Sheet

Add

Decrease in

Debtors

Stock

Prepiad expenses

Accrued income

Creditors

Increase in outstanding expenses

Debtors

Stock

Prepiad expenses

Accrued income

Creditors

Increase in outstanding expenses

Less

Increase in

debtors

Stock

Prepaid expenses

Accrued income

Decrease in creditors

Increase in outstanding expenses

Increase in

debtors

Stock

Prepaid expenses

Accrued income

Decrease in creditors

Increase in outstanding expenses

B3 profit and loss credit

Sales

Closing stock

By gross profit

Rent receive d

Income from investment s

Miscellaneous receipts

Net profit

B3 Profit and loss account Debit

Opening stock

Purchase s

Gross profit

Ad and selling expenditure

Debenture interest

Bank interest

Interim dividend

Proposed dividend

Renumeration

Provision for taxation

B3 Balance sheet Assets

Fixed assets

Good will

Buildings

Plant and mahinery

Less:depreciation

Investment s

Current assets

Interest on bonds

Current assets:

Stock in trade

Sundry debtor's

Less: provision for DD

loans and advances:

Miscellaneous expenditure

B3 Balance sheet liabilities

Liabilities

Share capital

Less: calls unpaid

By directors and others

Less: calls unpaid

By directors and others

Reserve and surplus

Less:debit balance in profit and loss account

Less:debit balance in profit and loss account

Secured loans

Unsecured loans

Unsecured loans

Current liabilities

Sundry creditors

Acceptance

Advance payments and unexpired discounts

Acceptance

Advance payments and unexpired discounts

Provisions

Bills payable

Sundry creditors

Debenture interest

Sundry creditors

Debenture interest

B3 Under subscription

In certain cases, The number of shares applied for may be less than the number of shares issued.

The the company will allot that much shares only.

Journal entry not required.

B3 over subscription

Some times the public may apply for more than the number of shares issued for subscription.

Directors may adopt

Rejecting applications

Alloting shares on prorata basis

Rejecting applications

Alloting shares on prorata basis

Wednesday, 8 June 2016

B3 Forfeiture of shares

Forfeiture of shares means

1. Cancellation of the membership of the share holder.i, e cancellation of share capital called upon the shares forfeited.

2. Forfeiture of whatever amount paid by the share holder in account of the share s forfeited.

2. Forfeiture of whatever amount paid by the share holder in account of the share s forfeited.

For bringing forfeited shares into effect in the books of account the following steps are needed.

a. The credit given to the share capital account to be debited with the amount of share capital called up in respect of those shares.

a. The credit given to the share capital account to be debited with the amount of share capital called up in respect of those shares.

b. The debits in the allotment, call account etc. Should be cancelled, for this the respective accounts should be credited with the amojnts due from share holders,

C, the amount already received from the shareholder is forfeited and transferred to shares forfeited account.

B3 Definitions

Authorized capital

The total or maximum amount of capital which the company authorized to raise

Called up capital

The total allotment of capital which the share holders are called upon to pay

Calls in Advance

The excess money paid by the share holders in respect to the share s alloted to him over and above what is payable before he is called upon to pay.

Calls in Arrears

The amount though called up the directors, the shareholders have failed to pay and thus in arrears.

Call money

When the directors inform thr shareholders to pay a apart of the share amount through a letter, it is said that a call has been made, the amount payable on such a call is called as call money.

B3 proforma Entries

Transaction and Entry

1.When share application money is received.

1.Bank account to share application account

2. On allotment o shares

A) For transfering share application money in respect of applications accepted

2a.Share application account to share capital account

B ) for allotment money due on allotment of shares

2b.Share allotment account to share capital account

3. On receipt of allotment money

3,Bank account to share allotment account

4. On making calls

A) for call money due on call

4a,Share call account to share capital account

B) on receipt of call money

4b.Bank account to share calls account

B3 Sources of Bonus shares

1. Share premium

2. Capital redemption reserve

3.General reserve

4.profit and loss account credit balance

5.capital profits such as profit prior to incorporation, profit on purchase of business, profit on sale of fixed assets etc and

6. Any other reserves accumulated out of profits.

B3 Objects of issuing Bonus Shares

1. To conserve the cash resources of the company

2. To present a proper figure of share capital with which profits can be compared

3. To offer capital gain to share holders.

Company issue bonus shares at the following circumstances-

1.when the company has accumulated large reserves,

2, when the company has expended such reserves in revenue producing assets and when it is not in a position to give cash bonus.

3, when there is a wide gap between the share capital and fixed assets. When the company is under capitalized.

B3 Bonus Shares

Bonus shares are those shares which are issued without any payment to the share holders. They are issued out of reserves, both capital and revenue. The process of issuing bonus shares is also known as capitalization of reserves.

B3 Realisation Account

It is the account which will be opened to close the business in he vendor company.

B3 AMALGAMATION

Takeover of business of two or more companies by a new company formed for the purpose,,

Tuesday, 7 June 2016

B3 BCIII 3 YEAR Procedure involved in raising the capital of a company

Raising the share capital of a company involves the following points:

a) Issue of a prospectus-inviting public to subscribe to its share capital.

b)Application for shares- receiving of applications and their scrutiny

c)Allotment and issue of shares to the shareholders.

d) Issue of shares to members.

a) Issue of Prospectus:

According to sec2(36) if the companies act. :prospectus means any document described or issued as prospectus and includes any notice, for the subscription of purchase of any shares in, or debentures of a body corporate.

b)Application for shares

a) Issue of a prospectus-inviting public to subscribe to its share capital.

b)Application for shares- receiving of applications and their scrutiny

c)Allotment and issue of shares to the shareholders.

d) Issue of shares to members.

a) Issue of Prospectus:

According to sec2(36) if the companies act. :prospectus means any document described or issued as prospectus and includes any notice, for the subscription of purchase of any shares in, or debentures of a body corporate.

b)Application for shares

Thursday, 4 February 2016

B1 Correlation

| Correlation Coefficient, r : |

the direction of a linear relationship between two variables. The linear correlation

coefficient is sometimes referred to as the Pearson product moment correlation coefficient in

honor of its developer Karl Pearson.

where n is the number of pairs of data.

(Aren't you glad you have a graphing calculator that computes this formula?)

linear correlations and negative linear correlations, respectively.

to +1. An r value of exactly +1 indicates a perfect positive fit. Positive values

indicate a relationship between x and y variables such that as values for x increases,

values for y also increase.

to -1. An r value of exactly -1 indicates a perfect negative fit. Negative values

indicate a relationship between x and y such that as values for x increase, values

for y decrease.

close to 0. A value near zero means that there is a random, nonlinear relationship

between the two variables

employed.

straight line. If r = +1, the slope of this line is positive. If r = -1, the slope of this

line is negative.

less than 0.5 is generally described as weak. These values can vary based upon the

"type" of data being examined. A study utilizing scientific data may require a stronger

correlation than a study using social science data.

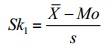

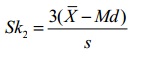

B1 Skewness by Karl Pearson

What is Pearson’s Coefficient of Skewness?

- Pearson’s Coefficient of Skewness #1 uses the mode. The formula is:

Where= the mean, Mo = the mode and s = the standard deviation for the sample.

See: Pearson Mode Skewness. - Pearson’s Coefficient of Skewness #2 uses the median. The formula is:

Where

It is generally used when you don’t know the mode.

Sample problem: Use Pearson’s Coefficient #1 and #2 to find the skewness for data with the following characteristics:

- Mean = 70.5.

- Median = 80.

- Mode = 85.

- Standard deviation = 19.33.

Pearson’s Coefficient of Skewness #1 (Mode):

Step 1: Subtract the mode from the mean: 70.5 – 85 = -14.5.

Step 2: Divide by the standard deviation: -14.5 / 19.33 = -0.75.

Step 1: Subtract the mode from the mean: 70.5 – 85 = -14.5.

Step 2: Divide by the standard deviation: -14.5 / 19.33 = -0.75.

Pearson’s Coefficient of Skewness #2 (Median):

Step 1: Subtract the median from the mean: 70.5 – 80 = -9.5.

Step 2: Divide by the standard deviation: -9.5 / 19.33 = -1.47.

Step 1: Subtract the median from the mean: 70.5 – 80 = -9.5.

Step 2: Divide by the standard deviation: -9.5 / 19.33 = -1.47.

Caution: Pearson’s first coefficient of skewness uses the mode. Therefore, if the mode is made up of too few pieces of data it won’t be a stable measure of central tendency. For example, the mode in both these sets of data is 9:

1 2 3 4 5 6 7 8 9 9.

1 2 3 4 5 6 7 8 9 9 9 9 9 9 9 9 9 9 9 9 10 12 12 13.

In the first set of data, the mode only appears twice. This isn’t a good measure of central tendency so you would be cautioned not to use Pearson’s coefficient of skewness. The second set of data has a more stable set (the mode appears 12 times). Therefore, Pearson’s coefficient of skewness will likely give you a reasonable result.

1 2 3 4 5 6 7 8 9 9.

1 2 3 4 5 6 7 8 9 9 9 9 9 9 9 9 9 9 9 9 10 12 12 13.

In the first set of data, the mode only appears twice. This isn’t a good measure of central tendency so you would be cautioned not to use Pearson’s coefficient of skewness. The second set of data has a more stable set (the mode appears 12 times). Therefore, Pearson’s coefficient of skewness will likely give you a reasonable result.

B1 Problems In The Construction Of Index Numbers

Problems In The Construction Of Index Numbers

Before constructing index numbers a careful thought must be given the following problems:1. The purpose of the index.

At the very outset the purpose of constructing the index must be very clearly, decided – what the index is to measures and why? There is no all-purpose index. Every index is of limited and particular use. Thus, a price index that is intended to measure consumers’ prices must not include wholesale prices. And if such an index in intended to measure the cost of living of poor families, great care should be taken not to include goods ordinarily used by middle class and upper-income groups.2. Selection of a base period.

Whenever index numbers are constructed a reference is made to some base period. The base period of an index number (also called the reference period) is the period against which comparisons are made.(I) THE BASE PERIOD SHOULD BE NORMAL ONE.

The period that is selected as base should be normal, i.e., it should be free from abnormalities like wars, earthquakes, famines, booms, depressions, etc. However, at times it is really difficult to select year which is normal in al respects – a year which is normal in one respect may be abnormal in another.(II) THE BASE PERIOD SHOULD NOT BE TOO DISTANT IN THE PAST.

It is desirable to have an index based on a fairly recent period, since comparison with a familiar set of circumstances is more helpful than comparison with vaguely remembered conditions.(III) FIXED BASE OR CHAIN BASE.

While selecting the base a decision has to be made as to whether the base shall remain fixed or not, i.e., whether we have a fixed base or chain base index.3. Selection of number of items.

The items included in an index should be determined by the purpose for which the index is constructed. Every item cannot be included while constructing an index number and hence once has to select a sample. It is also necessary to decide the grade or quality of the items to be included in the index. Index numbers shall give wrong result if at one time one set of qualities is included and at another time another set.4. Price quotations.

After the commodities have been selected, the next problem is to obtain price quotations for these commodities. It is a will known fact that prices of many commodities vary from place to place and even from shop to shop in the same market. It is impracticable to obtain price quotations from all the places where a commodity is dealt in. A selection must be made of representative places and persons. These places should be those which are well known for trading for that particular commodity.5. Choice of an Average.

Theoretically speaking, geometric mean is the best average in the construction of index numbers because of following reasons: (i) in the constructions of index number we are concerned with ratios of relative changes and the geometric mean gives equal weights to equal ratio of change; (ii) geometric mean is less susceptible to major variations as a result of violent fluctuations in the values of the individual items; and (iii) index numbers calculated by using the average are reversible and, therefore, base shifting is easily possible. The geometric mean index always satisfies the time reversal test.6. Selection of appropriate weights.

The problem of selecting suitable weights in quite important and at the same quite difficult to decide. The term ‘weight’ refers to the relative importance and hence it is necessary to devise some suitable method whereby the varying importance of the different items by taken into account. This is done by allocating weights. Thus, in the former case, no specific weights are assigned whereas in the latter case specific weights are assigned to various items. It may be pointed out here that no index is unweighted in strict sense of the term as weights implicitly enter the unweighted indices because we are giving equal importance to all the items and hence weights are unity. It is, therefore, necessary to adopt some importance to all the items and hence weights are unity. It is, therefore, necessary to adopt some suitable method of weighting so that arbitrary and haphazard weights may not affect the results. There are two methods of assigning weights: (i) implicit, and (ii) explicit.7. Selection of an appropriate formula.

A large number of formulae have been devised for constructing the index. The problem very often is that of selecting the most appropriate formula. The choice of the formula would depend not only on the purpose of the index but also on the data available.B1 Dispersion and skewness

S.No

|

Dispersion

|

Skewness

|

1

|

It is concerned

with measuring the amount of variation in a series rather than with its

direction

|

It is concerned

with the variation or the departure from symmetry

|

2

|

It tells us about composition of the

series

|

It tells about the shape of the

series

|

3

|

Measures of

dispersion are based on averages of the first order such as K, M, Z etc

|

Measure of skewness

arc based on averages of the first and second order such as X, M, Z etc

|

What is the difference between Dispersion and Skewness?

Dispersion concerns about the range over which the data points are distributed, and the skewness concerns the symmetry of the distribution.

Both measures of dispersion and skewness are descriptive measures and coefficient of skewness gives an indication to the shape of the distribution.

Measures of dispersion are used to understand the range of the data points and offset from the mean while skewness is used for understanding the tendency for the variation of data points into a certain direction.

B1 Limitation of statistics

The important limitations of statistics are:

(1) Statistics laws are true on average. Statistics are aggregates of facts. So single observation is not a statistics, it deals with groups and aggregates only.

(2) Statistical methods are best applicable on quantitative data.

(3) Statistical cannot be applied to heterogeneous data.

(4) It sufficient care is not exercised in collecting, analyzing and interpretation the data, statistical results might be misleading.

(5) Only a person who has an expert knowledge of statistics can handle statistical dataefficiently.

(6) Some errors are possible in statistical decisions. Particularly the inferential statistics involves certain errors. We do not know whether an error has been committed or not

Statistics

- Variable

- Characteristic or attribute that can assume different values

- Random Variable

- A variable whose values are determined by chance.

- Population

- All subjects possessing a common characteristic that is being studied.

- Sample

- A subgroup or subset of the population.

- Parameter

- Characteristic or measure obtained from a population.

- Statistic (not to be confused with Statistics)

- Characteristic or measure obtained from a sample.

- Descriptive Statistics

- Collection, organization, summarization, and presentation of data.

- Inferential Statistics

- Generalizing from samples to populations using probabilities. Performing hypothesis testing, determining relationships between variables, and making predictions.

- Qualitative Variables

- Variables which assume non-numerical values.

- Quantitative Variables

- Variables which assume numerical values.

- Discrete Variables

- Variables which assume a finite or countable number of possible values. Usually obtained by counting.

- Continuous Variables

- Variables which assume an infinite number of possible values. Usually obtained by measurement.

- Nominal Level

- Level of measurement which classifies data into mutually exclusive, all inclusive categories in which no order or ranking can be imposed on the data.

- Ordinal Level

- Level of measurement which classifies data into categories that can be ranked. Differences between the ranks do not exist.

- Interval Level

Level of measurement which classifies data that can be ranked and differences are meaningful. However, there is no meaningful zero, so ratios are meaningless. - Ratio Level

- Level of measurement which classifies data that can be ranked, differences are meaningful, and there is a true zero. True ratios exist between the different units of measure.

- Random Sampling

- Sampling in which the data is collected using chance methods or random numbers.

- Systematic Sampling

- Sampling in which data is obtained by selecting every kth object.

- Convenience Sampling

- Sampling in which data is which is readily available is used.

- Stratified Sampling

- Sampling in which the population is divided into groups (called strata) according to some characteristic. Each of these strata is then sampled using one of the other sampling techniques.

- Cluster Sampling

- Sampling in which the population is divided into groups (usually geographically). Some of these groups are randomly selected, and then all of the elements in those groups are selected.

Tuesday, 2 February 2016

Business Organisation and Management

22.Techniques of coordination:-

Sound planning

sound and simple organisation

chain of command

effective communication

committees

conferences

Social coordinaions

sound leadership

Problems of coordination:-

Uncertainity

Biological

Organisaional limits

Coordination:- orderly arrangement of group efforts to provide unity of action in the pursuit of a common purpose

Leaderahip:-process of influencing others towards the accomplishment of goals

21. Importance of controlling:

Aids planning

Improves efficiency

Aids decision making

Aids coordination

Improves

Techniques of control:-

Budgetary control

Standard Costing

Brrak-even analysis

PERT/CPM

Return on investment

Budget:- A blue print of a projected course of action, stated in quantitative terms.

Controlling:- The process of setting standard of performance measuring and comparing actual performance with the standard, taking corrective action when necessary

Friday, 29 January 2016

Thursday, 21 January 2016

Functions of Management

Functions of Management

1.Include planning organizing staffing directing controlling and coordinating

2.Planning which involve forecasting of future problems and event according to time

3.Organizing after deciding the objective and the ways and means of achieving them.

4.The next step is bringing together manpower and material resources required carrying out plan organisation resources are men material technology and finances in order to achieve enterprise objectives it involves decisions about the division of work allocation of authority and responsibility and coordination of tasks.

What is planning discuss the planning process in detail

Planning is defined as thinking before doing. the forecasting of future problems and events from you planning and decision making since planning required decision on :- what should be done

- how should be done

- Who will be responsible for doing it

- where is action to be taken

- Why is to be done

The planning is the function that determines in advance what should be done it consists of selecting the enterprise objectives policies programs procedures and other means of achieving objectives

line is regarded as one of the most important activities in organisation for 2 reasons as mentioned below

1.The dwindling natural resources for the management to think of having assured supplies for the production does not suffer

2.Rapid changes takes place in environment any other area. organisation how to cope up with changing environment and adapt dances to the changes for which planning is essential.

Types of planning

- According to the time Planning can be classified as short term plan which extend UPTo 1year

- Medium term plan of more than one year 5 years

- Long Term plan for 5 years or a long period

Multi use plan

- Objectives ,strategies, policies, procedures ,methods ,rules

- Single use plan

- Programs ,budgets ,project ,schedules

planning

State the meaning of communication . Explain steps in communication process?

What is planning discuss the planning process in detail

Planning is defined as thinking before doing. the forecasting of future problems and events from you planning and decision making since planning required decision on :- what should be done

- how should be done

- Who will be responsible for doing it

- where is action to be taken

- Why is to be done

The planning is the function that determines in advance what should be done it consists of selecting the enterprise objectives policies programs procedures and other means of achieving objectives

line is regarded as one of the most important activities in organisation for 2 reasons as mentioned below

1.The dwindling natural resources for the management to think of having assured supplies for the production does not suffer

2.Rapid changes takes place in environment any other area. organisation how to cope up with changing environment and adapt dances to the changes for which planning is essential.

Types of planning

- According to the time Planning can be classified as short term plan which extend UPTo 1year

- Medium term plan of more than one year 5 years

- Long Term plan for 5 years or a long period

Multi use plan

- Objectives ,strategies, policies, procedures ,methods ,rules

- Single use plan

- Programs ,budgets ,project ,schedules

Espirit de crops & Unity of command

Explain the following

Espirit de crops

It means that union is strength management should strive for harmony and understanding among the personnel .Unity among the members of staff is the greatest source of strength for the undertaking. Hence management should not indulge in divide and rule policy but should create Team Spirit employees. good communication system is must in order to Promote this in any organisation.

Unity of command

this principle states that employees should receive order from one superior only for any activity employees should not work under 2 bosses if they do so standards of performance may be affected, further any appreciation degree of discipline cannot be guaranteed.

Tuesday, 19 January 2016

Business Organisation & Management:Unit 20 Directing

|

S.no

|

Leadership

|

Managership

|

|

1

|

A

Leader May not have any formal authority, but he has power to influence

|

A

manager has formal authority which is granted by the organization

|

|

2

|

A

leader performs only the directing function

|

Manager

performs all the functions of a manager

|

|

3

|

Is elected

|

Is selected

|

|

4

|

May

have short term orientation

|

May

have long term orientation

|

Subscribe to:

Comments (Atom)

-

Benefits of GST | Advantages of Goods and Services Tax Updated on May 26, 2017 - 03:23:54 PM The Goods & Service Tax or GST ...